One of my favorite Saint Paul natives, F. Scott Fitzgerald, once wrote, “Let me tell you about the very rich. They are different from you and me.” But what is it that they do differently to grow and protect their wealth?

Here are a few things successful investors do better than most:

- Capture the Free Money: Many of us have access to a workplace retirement plan, and many of these plans offer employer matching contributions. Savvy investors always take full advantage of the matching funds their employer provides.

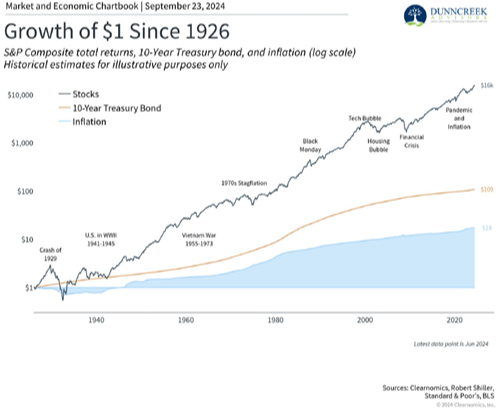

- Invest for Growth: For most families, the largest financial goal is retirement, and building enough wealth to cover future living expenses is critical. Many people don’t invest heavily enough in stocks within their retirement accounts. If you're at least five years away from retirement, you likely won’t need to access these funds for ten years or more. Therefore, stocks remain one of the best tools to grow your money faster than inflation.

Over the last 50 years, the S&P 500 index has averaged 11.92% per year with dividends reinvested, while corporate bonds have averaged around 6.1% over the last 30 years.

Have an Integrated Investment Strategy

Most of us have multiple “buckets” of savings. Each bucket requires a different investment strategy, and it’s essential that the overall strategy is coordinated and complementary. For example:

- Family Emergency Fund: This should be in a savings account at the bank. It’s not an investment—it’s insurance against unexpected bills.

- Family Vacation Fund: If you’re saving for expenses in the next 12 months, place this money in an interest-bearing account or a short-term investment fund.

- Kids’ College Fund: If you’re saving for five to ten years, consider a balanced and diversified investment fund.

- Retirement Fund: For money that will stay invested for 10 years or more, you can take a more aggressive approach with stocks to benefit from long-term growth.

All investments should be optimized with tax-smart strategies to maximize your family's spendable income.

Plan for Inflation

We’ve heard a lot about inflation recently, especially with the spike in today’s 4% inflation rate. However, the past decade saw unusually low inflation, which makes today’s rates feel more intense. Historically, since 1925, the U.S. cost of living has increased at about 3% per year. While today’s inflation is higher than we’re used to, it’s not drastically out of line.

Even at a 3% annual rate, the cost of living becomes significantly more expensive. A family that needs $4,000 per month today will need about $7,200 per month in 20 years and $9,700 per month in 30 years. To keep up with these rising expenses, your investments must outpace inflation to preserve the value of your savings.

Prepare for a Retirement Transition

As you approach retirement, it’s important to develop a game plan. I discuss three key dates in retirement planning with clients:

- The day you leave the Big Job: You plan to reduce income and stress, possibly transitioning to part-time work or consulting that’s more enjoyable. You may still earn enough to cover basic living expenses.

- The day you stop working entirely: This is when you no longer want to do any paid work and are comfortable living without earned income.

- The day you turn on your retirement income: This is when you start receiving pension distributions, Social Security benefits, or IRA withdrawals. You should be strategic about when to activate each income stream to maximize benefits.

In the five years leading up to leaving the Big Job, start building up cash in a brokerage account. Since this money isn’t bound by IRS retirement rules, you can access it easily and with less tax impact. This fund can provide you with months—or even years—of resources to smooth the transition from full-time work to full retirement.

Be Smart About Withdrawals

Most experts advise using your taxable brokerage account first, then tax-deferred IRA funds, and Roth IRA money last. However, your specific situation may vary. By projecting your income both during and after you quit the Big Job, you’ll have a clearer picture of which withdrawals best meet your needs.

Keep It Simple

Though there are plenty of variables, your overall approach should remain strategically simple. Aim to save about 20% of your earnings during your working years, invest in quality stock funds for long-term growth, and avoid making frequent changes to your investments.

Some people get caught up in investment fads or risky strategies like hedge funds and private placements because they feel behind and want to catch up. This can be risky. Like gambling, the urge to “double down” after losses can be tempting. Remember: slow and steady wins the race.

You might look at these seven ideas and think it’s a bit overwhelming. But, it doesn’t have to be. Maybe you should talk through these ideas with an experienced, highly-trained, CERTIFIED FINANCIAL PLANNER™ professional and Behavioral Financial Advisor in West Saint Paul, Minnesota to help better understand what makes sense for you. I love to meet new people. So, follow this LINK to find a time for us to have a get-acquainted visit.

I am a financial planner who is an advocate for my clients ALL THE TIME – a fiduciary financial planner. I provide guidance based on clients’ best interests, not commissions or sales quotas. I think it’s the best way to serve clients and I am thrilled to work this way all the time.

And yes, I’m still taking on a few great families to be part of my financial planning practice in West Saint Paul, Minnesota and, thanks to Zoom, across the country.

Dunncreek Advisors does not provide legal or tax advice, nor is this article intended to do so.